多変量時系列解析に関しては、最も広く知られているのはベクトル自己回帰 (VAR: Vector AutoRegressive) モデルである。

多変量時系列の標本データを

とすると(誘導型)VARモデルは次のように定義される。

モデルの中の係数A1,A2,…,Apは行列、 残差Etはベクトルである。

VARモデルを推定するためには、2種類の方法がある。 パッケージtseriesを利用するか、VARモデル専用のパッケージである、varsを利用するかである。

1)パッケージtseriesの利用

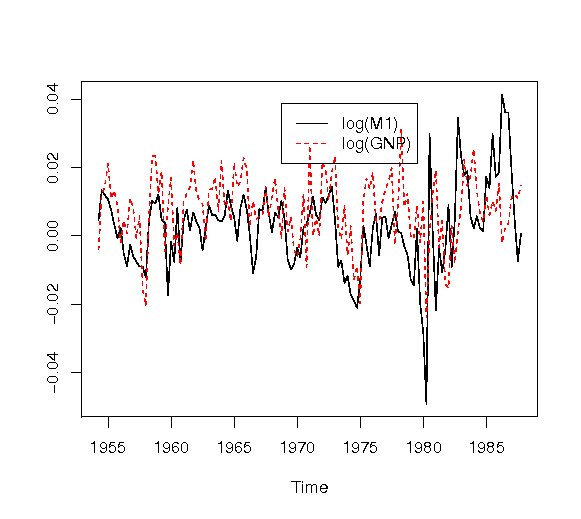

1つ目は、tseriesを用いて、その中に入っているarima関数または、ar関数を用いる方法である。 ここではパッケージtseriesの中に用意されている、 1954年の第1四半期から1987年第4四半期までのアメリカの4 変量の経済時系列データUSeconomicの中の先頭の2変量を用いる。 第1変量はlog(GNP)=実質GNP の対数値(季調済み)、第2変量はlog(M1)=実質M1 の対数値(季調済み)である。 データにはトレンドがあるので、1階差分を取って用いる。

> library(tseries); > data(USeconomic) > USe.d<-diff(USeconomic[,1:2]) > ts.plot(USe.d,lty=c(1,2),col=c(1,2)) > legend(locator(1),c(colnames(USe.d)[1],colnames(USe.d)[2]),lty=c(1,2),col=c(1,2)) |

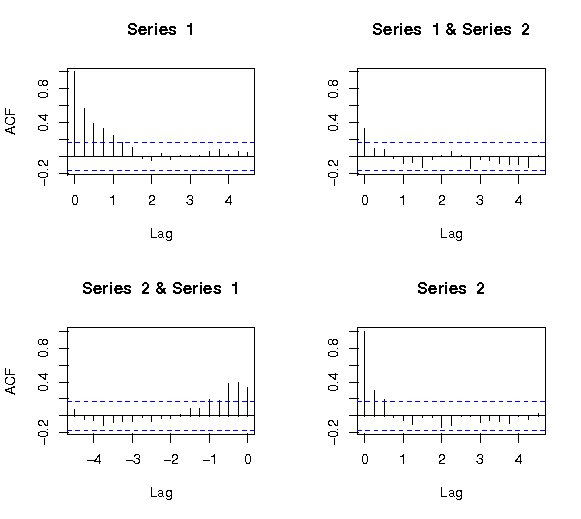

自己相関は、単変量の場合と同じく次のように関数acfで求めることができる。

> acf(USe.d, na.action=na.pass) |

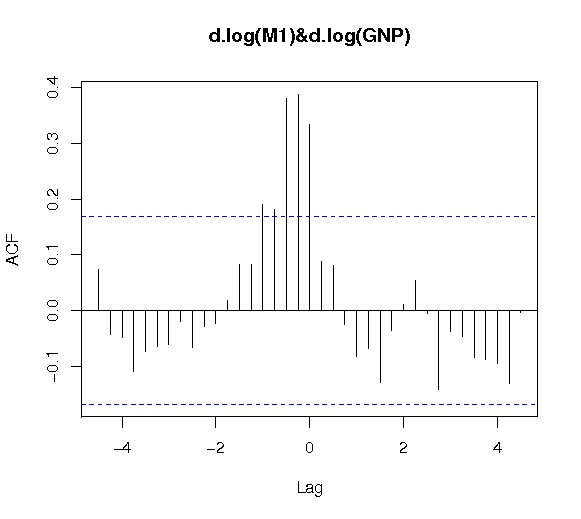

また、相互相関は、次のように関数ccfで求めることができる。

>ccf(USe.d[,1],USe.d[,2],main="d.log(M1) & d.log(GNP)") |

関数arを用いたVARモデルを当てはめる例を次に示す。 関数arでは、引数aic=TRUEで計算すると自動的に最適な次数の推定値に基づいて結果を返す。 ここでは、返す結果とモデルの対応関係を説明するため、 次のように強制的にVAR(2)モデル(必ずしも最適なケースではない)の推定値を求める。

> (USe.ar<-ar(USe.d,order.max=2,aic=F))

Call:

ar(x = USe.d, aic = F, order.max = 2)

$ar

, , 1

[,1] [,2]

[1,] 0.5446 -0.1888

[2,] 0.1981 0.1295

, , 2

[,1] [,2]

[1,] 0.1231 0.04513

[2,] 0.1371 0.07110

$var.pred

[,1] [,2]

[1,] 1.063e-04 1.506e-05

[2,] 1.506e-05 8.494e-05

|

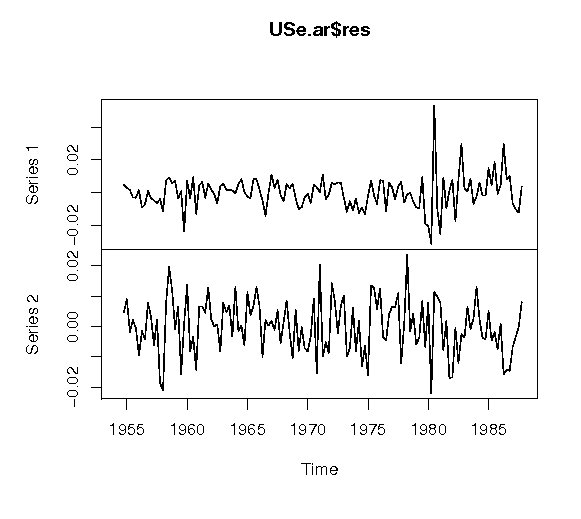

返された結果を用いた2変量のモデルを次に示す。

式の中のMはlog(M1)の1階差分値で、Mはlog(GNP)の1階差分値である。残差のプロットを次に示す。

> plot(USe.ar$res)) |

作成したモデルの予測値は次のように求めることができる。 ただし、現在のバージョンでは多変量時系列の予測値の推定標準誤差は計算できないので、se.fit=Fにする。

> USe.f<-predict(USe.ar,n.ahead=12,se.fit=F) |

2)パッケージvarsの利用

> library(vars)

> v1<-VAR(USe.d,p=1,type="const")

> summary(v1)

VAR Estimation Results:

=========================

Endogenous variables: log.M1., log.GNP.

Deterministic variables: const

Sample size: 134

Log Likelihood: 865.363

Roots of the characteristic polynomial:

0.4715 0.323

Call:

VAR(y = USe.d, p = 1, type = "const")

Estimation results for equation log.M1.:

========================================

log.M1. = log.M1..l1 + log.GNP..l1 + const

Estimate Std. Error t value Pr(>|t|)

log.M1..l1 0.605185 0.075740 7.990 6.09e-13 ***

log.GNP..l1 -0.142638 0.093215 -1.530 0.128

const 0.002032 0.001112 1.827 0.070 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.01033 on 131 degrees of freedom

Multiple R-Squared: 0.3327, Adjusted R-squared: 0.3225

F-statistic: 32.66 on 2 and 131 DF, p-value: 3.103e-12

Estimation results for equation log.GNP.:

=========================================

log.GNP. = log.M1..l1 + log.GNP..l1 + const

Estimate Std. Error t value Pr(>|t|)

log.M1..l1 0.2644613 0.0678459 3.898 0.000154 ***

log.GNP..l1 0.1893458 0.0834998 2.268 0.024990 *

const 0.0055944 0.0009962 5.616 1.12e-07 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.00925 on 131 degrees of freedom

Multiple R-Squared: 0.1842, Adjusted R-squared: 0.1717

F-statistic: 14.79 on 2 and 131 DF, p-value: 1.622e-06

Covariance matrix of residuals:

log.M1. log.GNP.

log.M1. 0.0001066 1.750e-05

log.GNP. 0.0000175 8.557e-05

Correlation matrix of residuals:

log.M1. log.GNP.

log.M1. 1.0000 0.1832

log.GNP. 0.1832 1.0000

|

構造型VARモデルの推定

Aが非特異であるならば、両辺に左より逆行列をかけることにより、 誘導型VARモデルに変換する事ができる。

Granger因果性とインパルス応答関数

> varset<-read.table("varset.txt",header=T)

> ci<-varset[,2]

> cpi<-varset[,3]

> call<-varset[,4]

> lci<-100*log(ci)

> lcpi<-100*log(cpi)

> dci<-100*diff(log(ci))

> set<-data.frame(lci,lcpi,call)

> v1<-VAR(set,p=1,type="const")

> summary(v1)

VAR Estimation Results:

=========================

Endogenous variables: lci, lcpi, call

Deterministic variables: const

Sample size: 115

Log Likelihood: -123.391

Roots of the characteristic polynomial:

0.9506 0.9506 0.9221

Call:

VAR(y = set, p = 1, type = "const")

Estimation results for equation lci:

====================================

lci = lci.l1 + lcpi.l1 + call.l1 + const

Estimate Std. Error t value Pr(>|t|)

lci.l1 0.97007 0.01527 63.535 < 2e-16 ***

lcpi.l1 -0.30549 0.11070 -2.760 0.00677 **

call.l1 -0.44240 0.10051 -4.401 2.48e-05 ***

const 155.23398 51.46163 3.016 0.00317 **

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.8835 on 111 degrees of freedom

Multiple R-Squared: 0.9734, Adjusted R-squared: 0.9727

F-statistic: 1354 on 3 and 111 DF, p-value: < 2.2e-16

Estimation results for equation lcpi:

=====================================

lcpi = lci.l1 + lcpi.l1 + call.l1 + const

Estimate Std. Error t value Pr(>|t|)

lci.l1 0.004363 0.005809 0.751 0.4541

lcpi.l1 0.890746 0.042112 21.152 <2e-16 ***

call.l1 -0.061823 0.038239 -1.617 0.1088

const 48.559615 19.577614 2.480 0.0146 *

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.3361 on 111 degrees of freedom

Multiple R-Squared: 0.9623, Adjusted R-squared: 0.9613

F-statistic: 945.4 on 3 and 111 DF, p-value: < 2.2e-16

Estimation results for equation call:

=====================================

call = lci.l1 + lcpi.l1 + call.l1 + const

Estimate Std. Error t value Pr(>|t|)

lci.l1 0.0006135 0.0025719 0.239 0.812

lcpi.l1 0.0036994 0.0186468 0.198 0.843

call.l1 0.9623283 0.0169317 56.836 <2e-16 ***

const -1.9855258 8.6687166 -0.229 0.819

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.1488 on 111 degrees of freedom

Multiple R-Squared: 0.9939, Adjusted R-squared: 0.9937

F-statistic: 5992 on 3 and 111 DF, p-value: < 2.2e-16

Covariance matrix of residuals:

lci lcpi call

lci 0.780550 -0.028677 0.006348

lcpi -0.028677 0.112967 -0.005527

call 0.006348 -0.005527 0.022148

Correlation matrix of residuals:

lci lcpi call

lci 1.00000 -0.09657 0.04828

lcpi -0.09657 1.00000 -0.11049

call 0.04828 -0.11049 1.00000

> causality(v1,cause="call")

$Granger

Granger causality H0: call do not Granger-cause lci lcpi

data: VAR object v1

F-Test = 11.7903, df1 = 2, df2 = 333, p-value = 1.129e-05

$Instant

H0: No instantaneous causality between: call and lci lcpi

data: VAR object v1

Chi-squared = 1.547, df = 2, p-value = 0.4614

|

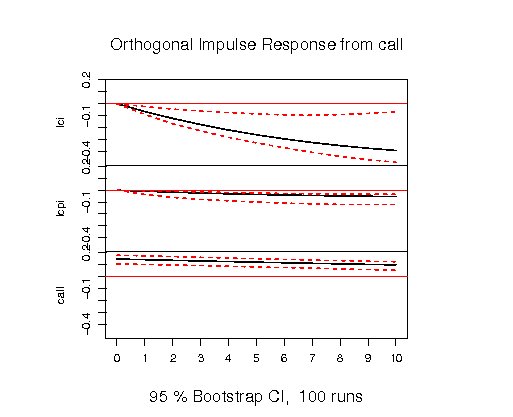

インパルス反応関数

> impulse<-irf(v1,impulse="call",response=c("lci","lcpi","call"),boot=TRUE)

> plot(impulse)

|

実線がインパルス応答関数であり、破線はブートストラップ法により求めた95%信頼区間である。 一番上の図は、callのインパルスに対して、lciは遅れて有意に負の反応を示す。 同様に、callのインパルスに対して、lcpiも有意に負の反応をしている。 一方、callのインパルスに対して、call自身は、始めは正の反応をしているものの、 その影響は次第に薄れていく事を示している。

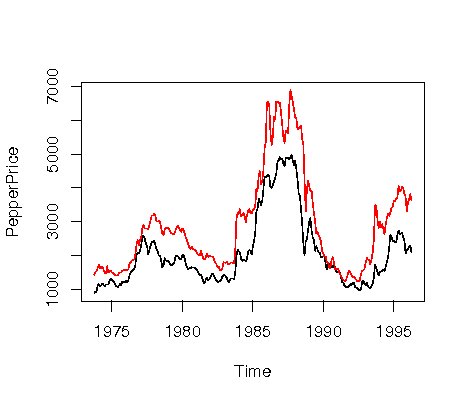

共和分

短期的には異なることもあるが、長期的には同じ動きをするような2つ以上のデータがある場合、 共和分関係にあるといわれている。 まず共和分関係にあるかどうかを調べる関数として、po.test()がある。

> library(AER)

> data("PepperPrice")

> plot(PepperPrice,plot.type="single",col=1:2)

> library(tseries)

> po.test(log(PepperPrice))

Phillips-Ouliaris Cointegration Test

data: log(PepperPrice)

Phillips-Ouliaris demeaned = -24.0987, Truncation lag parameter = 2,

p-value = 0.02404

|

これから統計量が負であり、絶対値が十分大きいことから, この2つのデータは共和分関係であることを示している。 詳しくはHamilton, J.W.「時系列解析〈下〉非定常/応用定常過程編」

この関係にある場合には、Grangerの表現定理(Granger and Engle(1987))から誤差修正モデル(Error Correction Model)に帰着することが知られている。これを調べるにはco.jo()の関数が知られている。

> library(urca)

> pepper_jo<-ca.jo(log(PepperPrice),ecdet="const",type="trace")

> summary(pepper_jo)

######################

# Johansen-Procedure #

######################

Test type: trace statistic , without linear trend and constant in cointegration

Eigenvalues (lambda):

[1] 4.931953e-02 1.350807e-02 2.081668e-17

Values of teststatistic and critical values of test:

test 10pct 5pct 1pct

r <= 1 | 3.66 7.52 9.24 12.97

r = 0 | 17.26 17.85 19.96 24.60

Eigenvectors, normalised to first column:

(These are the cointegration relations)

black.l2 white.l2 constant

black.l2 1.0000000 1.00000 1.000000

white.l2 -0.8892307 -5.09942 2.280911

constant -0.5569943 33.02742 -20.032441

Weights W:

(This is the loading matrix)

black.l2 white.l2 constant

black.d -0.07472300 0.002453210 2.697730e-17

white.d 0.02015611 0.003537005 3.401573e-18

|

Back to R